Author: Richard Yasenchak, CFA, CFP®, Senior Managing Director, Head of Client Portfolio Management

Cap-weighted indexes potentially embed concentrated risk. Explore why fiduciaries must govern how core equity is structured, not just what they own.

For years, core U.S. equity exposure has been treated as investment policy neutral.

It seeks to anchor investment policy statements.

It attempts to define beta.

It is often implemented as “passive.”

But passive does not mean riskless. And it no longer means diversified in the way many fiduciaries assume.

Cap-weighted equity exposures are increasingly difficult to treat as a neutral policy default. Concentration and characteristic drift have increased the sensitivity of passive allocations to index leadership and style cycles

When a small group of stocks drives a disproportionate share of return and risk, the exposure may still track an index, but structurally, it begins to behave like a concentrated strategy.

That shift changes the fiduciary conversation.

Ownership Is Not the Same as Risk

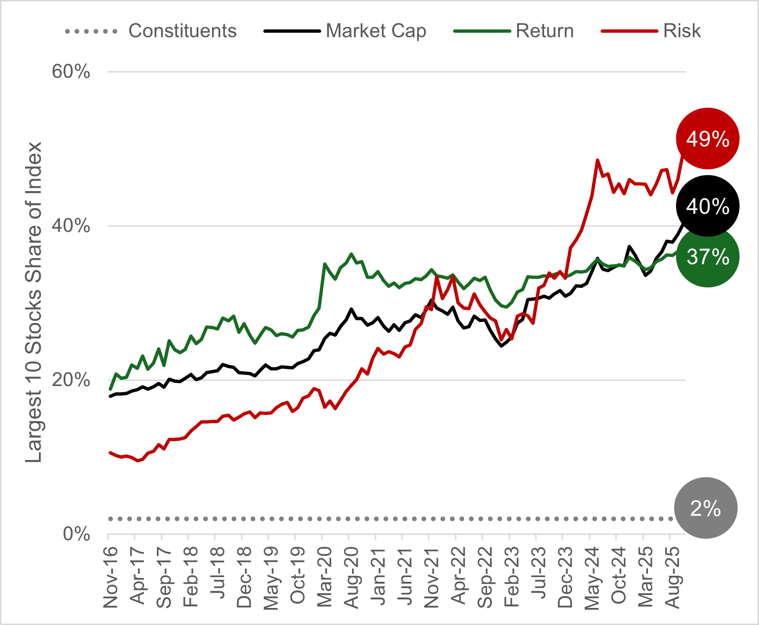

Most concentration discussions focus on market-cap weights. But the more important question is risk contribution. As of December 31, 2025, the 10 largest stocks in the S&P 500® Index represented approximately:

- 2% of constituents

- 40% of market capitalization

- 37% of cumulative return contribution

- 49% of total risk contribution

That final figure is the governance issue.

When half of index risk comes from a handful of names, the portfolio may look diversified by count — but not by influence.

Broad Exposure, Concentrating Risk.

Source: FactSet. Reflects monthly contributions of constituents, market capitalization, return, and risk for the 10 largest stocks within the S&P 500® Index for the 10 years ended December 31, 2025. Concentration levels change over time and may be higher or lower in the future. Charts are for illustrative purposes only and do not represent actual performance of any Intech strategy. Past performance is not indicative of future results. Indices are unmanaged, do not reflect fees, and are not available for direct investment.

This is not a forecast. It is observable structure.

The Problem Is Structural, Not Cyclical

Markets rotate. Leadership changes. Cycles normalize. But the design of cap-weighted indexes does not change. Core equity risks today are driven more by strategy construction — concentration, characteristic drift, and style-cycle sensitivity than by short-term market noise. In other words, the issue is how strategies are built.

Consider the potential structural trade-offs embedded in common core approaches:

- Cap-weighted indexes: Concentrate capital in the largest companies.

- Equal-weighted variations: Tilt toward smaller, more volatile stocks.

- Active managers: Concentrate in high conviction names.

- Factor strategies: Concentrate in defined characteristics.

Each redistributes risk differently. None eliminate concentration. They simply shift where it resides. The fiduciary question becomes: Is that redistribution intentional and documented, or inherited by default?

When Does Passive Start Behaving Like Active?

Investment policy statements often treat passive core allocations as baseline exposure — stable, diversified, low-maintenance.

But when leadership narrows and correlations shift, cap-weighted portfolios naturally drift toward dominant names. Exposure builds mechanically. Risk compounds silently. No one votes to concentrate. It simply happens.

In such environments, exposure exhibits characteristics akin to a concentrated strategy — not because someone selected it, but because structure delivered it.

For fiduciaries, implicit bets require additional oversight. Not because they are wrong. Because they are undocumented.

Governance Requires a Process

The duty is not to abandon the benchmark. Most institutional frameworks require it. The duty is to recognize that when risk becomes measurable, it warrants structured oversight. Core equity is no longer a static exposure. It is a design. And design requires:

- Monitoring concentration and risk contribution

- Understanding how correlations affect diversification

- Evaluating how portfolios evolve as prices move

- Maintaining an audit trail for how risk is managed

The benchmark hasn’t changed. What has changed is how much risk is embedded in it.

Diversification Is Not a By-Product

Many investors assume diversification happens automatically inside an index. But diversification is not a by-product of inclusion. It is a function of how weights, correlations, and rebalancing interact over time. When concentration builds, diversification erodes, even if the portfolio still holds hundreds of names.

The question is not:

“Are we indexed?”

The question is:

“How is risk distributed inside our core allocation?”

What Comes Next

We believe there is a systematic way to maintain benchmark alignment while redistributing risk more deliberately. It begins by reframing how portfolios grow, not just through business fundamentals, but through portfolio structure. It integrates measurable stock characteristics with disciplined construction and rebalancing.

And it operates within defined constraints on tracking error, sector exposure, liquidity, and turnover But before discussing the mechanism, the governance question must be clear. If core equity is behaving like a concentrated strategy, is it being governed like one?

For Fiduciaries, Clarity Is Defense

When risks are visible and quantifiable, they require oversight.

Not reaction.

Not prediction.

Oversight.

Core equity does not have to be abandoned to be governed. But it does need to be examined through the lens of structure, not just cost. The benchmark still defines what you own. The real fiduciary decision is how you own it.

Explore the Full Framework

Download the paper to see how portfolio structure can be engineered alongside benchmark exposure - within a systematic, documented process designed for fiduciaries.